Monday, November 29, 2010

Yesterday saw the finalization of the E 85 bn rescue package for Ireland. There are many interesting parts about it, but what stood out to me was the fact that it was basically a bank bail-out. The Irish treasury had diligently stacked away a cash pile to help them over the worst refinancing needs next year and together with their already severe austerity package they seemed good for at least one winter and half a summer.

So what was the problem? The major problem was a slumbering banking crisis that did not want to go away. Like so many of the European tigers, Ireland had had a recent history of unprecedented growth. A large part of the growth was related to construction both for residential and commercial property. This was, not unlike the US and Spain, largely financed by the banks in ever increasingly aggressive mortgage structures. Historically low interest rates fueled the demand - mortgage demand seemed unlimited, with ever increasing house prices and good rental yields. The supply was also unlimited as the Irish banks could attract cheap funding form other European banks and the bond markets.

The mortgage party came to an abrupt halt late in 2007, when inter-bank funding and bond markets dried up. Banks became scared of lending to banks as the banking crisis unfolded and bond holders became vary of putting money into what seemed opaque financial institutions. The time bomb that transpired was overleveraged mortgages markets in nearly all developed markets. In the case of the Irish markets, the initial panic of depositors was stilled with a blanket guarantee on deposits. That guarantee is still in place.

The real challenge, however, was still to come as inter-bank funding started to dry up and bond maturities were not rolled-over. The only remaining recourse left was the European Central Bank (ECB). In August 2007 the ECB started funding the banks with short term funds. By September 2010, in the case of Ireland, this amounted to more than E 100 bn in funding. Clearly this was an untenable situation that could not be perpetuated indefinitely. The ECB was uncomfortable with the situation, the European Commission was unconformable with the situation, and the bond market was very uncomfortable with the situation. And now just over three years later, a more structural solution via the Irish government was basically forced onto the Irish banks.

So what does all of this mean for Spain and Spanish banks? Well, clearly there are lots of parallels and lots of differences between the two countries, their banks and their economies. The differences are manifest: Spain is much less indebted than Ireland; Spain is much less dependent on foreign bondholders and financiers than Ireland; Spain has a number of large system banks that are much more solvent and bankable than Ireland; Spain is a much larger and economy than Ireland. To give you an idea, Spain has an economy of just over E 1 trillion and Ireland one of just under E 160 bn. Spain’s government debt represents 53% of GDP and Ireland’s 65.5% (end 2009)

On the other hand there are a number of very uncanny similarities:

1. The Spanish economic boom of the past years has also been fueled by the construction sector.

2. A large portion of the Spanish banking sector, especially the savings banks called the Cajas, is also largely funded by the ECB. The outstanding liabilities of the ECB vis-à-vis the Spanish banking sector is a whopping E 68 bn.

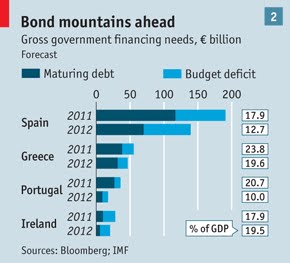

3. The Spanish banking sector has substantial redemptions in the coming 3 years with more than E 50 bn due in 2011 and more than E 100 bn due in 2012.

4. Foreign banks have claims in excess of E 656 bn on Spain that range from inter-bank funding, to direct operation in the local market, not to forget to exposure to local covered bonds (cedulas).

A huge amount in other words, but Spain has taken a number of drastic measures to address the crisis:

1. Like most other PIIGS it has put in place an extensive austerity package.

2. Labor markets have been made more flexible, with the hope to eventually see unit labor cost drop and competitiveness increase.

3. The restructuring of the savings banks have been started in all earnest.

Seemingly, like with the Ireland, the real issue will be to assess the size of the liquidity required by the Spanish banking sector, and more specifically the Cajas in the coming months and years. As previously mentioned the sovereign debt levels of Spain is not out of proportion big vis-à-vis the Spanish economy. The sovereign redemptions and additional sovereign issuance of Spain is daunting for 2011 at around E 75 bn, but given the size of the economy and extent of local investors, this would seem digestible.

So what is the situation with the Cajas? A Fund for the Orderly Restructuring of the Banking system of E 99 bn has been put in place. The Cajas have been cajoled into merging into more solid and digestible blocks and to start extensive restructuring of their costs and loan books. The Cajas are reported to have E 76 bn in the capital, with an assumed core tier one of around 8%, it brings their combined total balance sheets to around E 1 trillion. Say approximately 7% of that use to be funded via the interbank market (E 70 bn) and 18% (E 180 bn) of that is being funded via the covered bond market. This would mean that the immediate funding requirement of the Cajas is somewhere between E 70 bn and E 240 bn. A portion of this could be absorbed the recapitalization of the Cajas and a portion of this is being finance via the ECB short term lending facility, seemingly close to E 68 bn (reported by BIS).

What could this mean for Spain in terms of extra government debt in the coming years?

1. Spain needs between E 20 -25 bn per annum in new sovereign issuance in the coming 3 years

2. Spain would need a further E 70 bn in government debt to replace the ECB short term funding to the Cajas

3. Spain might need up to E 180 bio in covered bonds in the Cajas that mature in the coming 3 years and might not be rolled-over.

4. Add this to the existing debt of Spain of E 560 bn, one quickly ends up with an amount of Spanish government debt close to E 900 bn in 2013, a whopping 85% of GDP in 2013.

This figure is rather extreme and the likelihood that the covered bond market (“cedulas” market) and interbank will dry up completely is probably unlikely, making a more realistic sovereign debt level in Spain somewhere between E 600 and 700 bn by 2013.

What can we learn form this? First of all, that a sound banking system with a normalized inter-bank market is a critical part of the solution of the European sovereign debt problem. Second of all, acceptable sovereign debt levels today do not mean that there is no need for European bail-out funding support. Third of all, the ECB plays a critical part in indirectly supporting European governments at this moment – a role the ECB does not feel comfortable filling at all! So watch the statements by the ECB top closely!

Geen opmerkingen:

Een reactie posten

It spring again in old Amsterdam. It is still too early for the tulips, but there are already thousands of little crocuses on every roundabout! Spring is such a lovely time. Having grown up in sunny South Africa, with its near eternal summers, one never realizes the full significance of spring in the cold North! The little green dots in the grey bushes, the tiny specs of color in the fields herald a new beginning and a thankful ending.